Input VAT apportionment: BMF letter dated 13 February 2024

ServicesTaxGlobal Indirect Tax - Value Added Tax and CustomsLatest VAT News

Input VAT apportionment: BMF letter

The right to deduct input VAT only exists if an input supply is used for a taxed output turnover.

If an input supply cannot be directly and immediately allocated to a specific output turnover, but only to the business activity as a whole, an input VAT ratio must be calculated by comparing the taxed turnover to the total turnover. The Federal Ministry of Finance has issued several clarifications to the administrative guidelines of the German VAT Code (UStAE).

If an input supply cannot be directly and immediately allocated to a specific output turnover, but only to the business activity as a whole, an input VAT ratio must be calculated by comparing the taxed turnover to the total turnover. The Federal Ministry of Finance has issued several clarifications to the administrative guidelines of the German VAT Code (UStAE).

Background: § 15 para. 4 sentence 2 UStG must be teleologically reduced in line with EU law

§ 15 para. 4 sentence 2 UStG (German VAT Code) stipulates that a turnover key (i.e. a total turnover key) may only be selected if no other economic allocation is possible. In contrast, Art. 173 of the VAT Directive assumes that the total turnover key is the general rule, but the Member States may deviate from this. ECJ case law stipulates that a key other than the total turnover key may only be required if it leads to more precise results. The BFH (German Federal Fiscal Court) has subsequently ruled that

§ 15 para. 4 sentence 2 UStG must be interpreted as meaning that a total turnover key may only be used if there is no other allocation method that provides more precise results.

The main provisions of the BMF letter

- Turnover keys that are not linked to the company’s total turnover (e.g. object or department-related partial turnover keys) can also be a "different economic allocation" within the meaning of § 15 para. 4 sentence 2 UStG and thus take precedence over a total turnover key if they are more precise.

- The taxable person can choose from several keys that are more precise than the total turnover key and does not necessarily have to use the most precise one.

- Exception: In the case of mixed-use buildings, the area key also generally takes precedence over an object-related turnover key. This corresponds to the previous view taken by the tax authorities as documented in the BMF letter of 20 October 2022 (as we reported here) and is a considerable disadvantage for the real estate sector because commercial rents that entitle the taxpayer to deduct input VAT are generally significantly higher than VAT exempt residential rents.

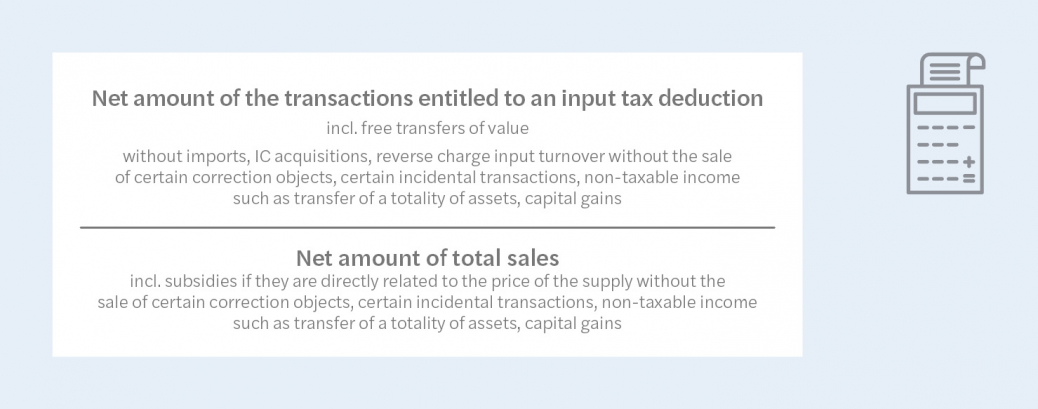

- The total turnover key results from the following break:

- In the case of margin taxation for travel services (§ 25 UStG) and differential taxation (§ 25a UStG), the sales price less VAT must also be taken into account in the break, not just the margin/difference.

- For the time allocation of the output sales in the break, the time at which the tax accrues and, if applicable, the change in the assessment basis according to § 17 UStG as well as the regulations regarding taxation based on payments agreed according to § 20 UStG must be observed.

- The rounding up of the percentage of deductible input VAT to full percentage points in accordance with Art. 175 (1) of the VAT Directive is only permitted for the total turnover key. All other keys must be rounded up to two decimal places.

- The total turnover key may be used in the preliminary VAT returns (e.g. based on the previous year’s key) but must then be corrected on the annual VAT return.

- In the case of correction objects within the meaning of § 15a UStG, the requirements for an input VAT adjustment in accordance with § 15a must be reviewed annually within the correction period. If the percentage of deductible input VAT was rounded up to full percentage points when the input VAT was claimed in accordance with recital 13 of the BMF letter, the percentage of deductible input VAT must also be rounded up to full percentage points during the entire correction period, irrespective of the method used in the correction year.

The principles of this BMF letter are to be applied in all open cases. The UStAE is amended accordingly. The BMF letter of 20 October 2022 on input VAT deduction for mixed-use buildings continues to apply as well. Among other things, it defines the exceptions in which the property-related area key is not appropriate.

Author

Nadia Schulte

+49 211 83 99 330

Contact

Birgit Jürgensmann Partner Düsseldorf

Thomas Pelzer Director Tax Berlin

Stephanie Stahl Senior Manager Berlin