Want to know more?

Even before the result of the Brexit referendum, 2016 was an uncertain year for construction in Europe. First quarter publications from the 15 major European construction groups reflect these uncertainties, with an average fall in activity of 5%.

However Construction in Europe has shown signs of recovery for the past two years and has been growing faster than GDP, led by growth in the housing sector (+ 2.8%) and public works sector (+ 6.2%) in 2015.

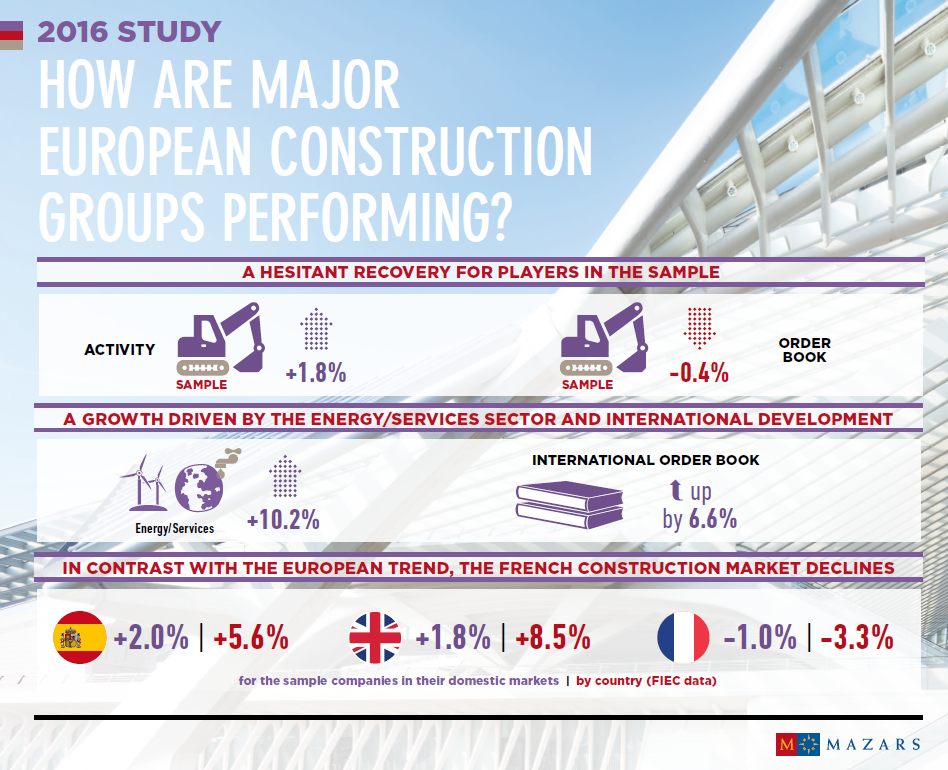

Against this background of recovery, major European construction groups have also returned to growth (+1.8%) following two years of contraction, due to strong growth in energy and services (+10.2%) and to the international development of the groups, with international order books rising by 6.6%.

Find out more in our study below.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.