Want to know more?

As part of the Corona economic stimulus package, Germany‘s ruling parties have agreed on a temporary reduction of VAT rates: Accordingly, in the period from July 1 to December 31, 2020, the standard tax rate is reduced from 19% to 16% and the reduced VAT rate from 7% to 5%.

The implementation of this measure has presented companies with enormous challenges in the recent weeks. How extensive were the changes for companies and how did they deal with this challenge? What experiences did they have in business operations, for example in dealing with other companies or customers? And finally: Has the original goal of the tax rate reduction – a strong stimulus on demand – been achieved? Have sales in the companies developed positively?

In our short survey, we have focused on questions like these and compiled the results for you in our study report.

How can the results be interpreted? Find out more in our short Q&A with our VAT expert Birgit Jürgensmann, lawyer, tax consultant, specialist in tax law and partner at Mazars.

1. Were there any surprises in the results?

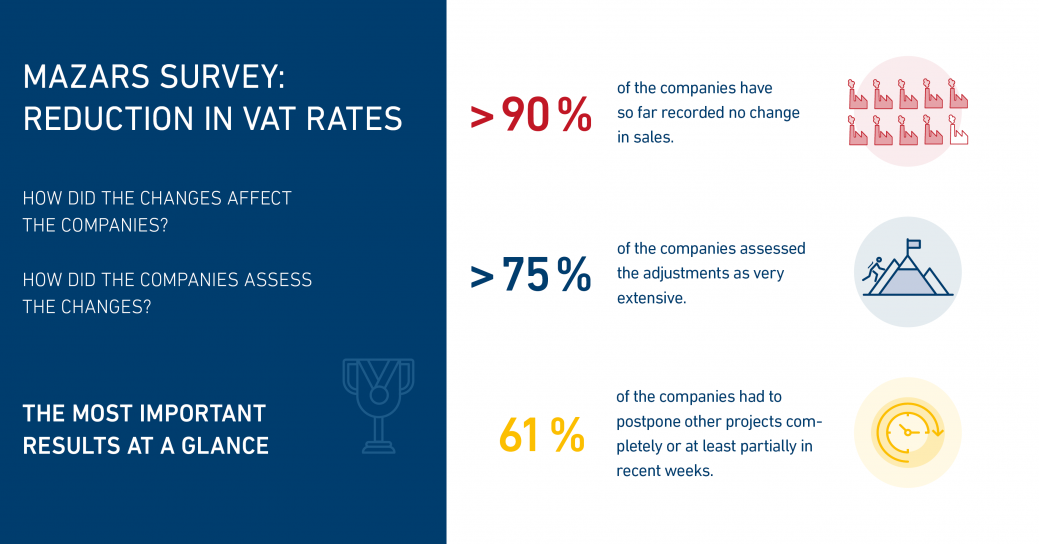

“There were no real surprises. Rather, our experiences from daily practice were confirmed by the survey. However, the figures in absolute terms – more than 90% of the companies had no changes in sales, for more than 75% of the companies the necessary adjustments were very extensive and 61% of the companies had to postpone other projects completely or at least partially – those facts should set us thinking.”

2. What is the impact of postponing other projects for the companies?

“The fact that almost two thirds of the companies had to postpone other projects due to the reduction in VAT rates is a worrying sign in our view. In practice, we believe that companies are currently only able to meet the high demands of legal changes in the field of VAT law to a limited extent. On January 1, 2020, the so-called "Quick Fixes" were introduced, with stricter controls on VAT identification numbers and recapitulative statements, from mid-March, the "corona lockdown" with deferral applications, possibly other sales tax options to improve liquidity in the corona crisis (e.g. staggered target taxation) and adjustments to the supply chain required full concentration, and from the beginning of June, the reduction of VAT rates was on the agenda of companies. The outlook for the future shows that the work in the tax departments is not diminishing: As things stand at present, VAT rates are to be returned to the original rates by January 1, 2021, and the (potentially) "hard" Brexit must be put into practice. The implementation of the "EU Commerce Package" is also on the to-do list. In view of the high expectations of the tax authorities regarding the tax compliance of a company as well as the strict procedure in the event of infringements, this is a matter of great concern to many.”

3. How do you think will the situation for companies develop?

“The challenges for companies are considerable in the field of VAT law alone, as just mentioned. The immense tax losses due to the corona measures taken, suggest that tax audits worldwide will be much more stringent in future.

However, the current framework conditions also offer companies the opportunity to analyze, adapt and optimize their business models and their implementation in processes. We regularly discover that certain processes were introduced in the past based on a single order, but that these no longer make sense at present.

In connection with the reduction of the VAT rate, many companies had to find out that the practical handling was not in accordance with the contractual regulations. In a situation like this, companies should eliminate risks by harmonizing practices and contracts.

For many companies, the corona situation means an adjustment of 'sourcing', which is accompanied by changes in the supply chain. Every change in the supply chain in turn has effects from a sales tax and customs perspective.

With all these topics, considerable costs can be caused, e.g. through no longer necessary sales tax registrations and associated administrative obligations, elimination of warehouses, optimized transport routes, use of customs privileges. Simplified supply chains also mean that the demands on the technical know-how of employees are at a 'normal' level, rather than requiring special expertise.

We know from quite a few companies that due to the considerable liability risks for acting persons, positions in tax and accounting are increasingly difficult to fill. A well-established tax compliance management system can help to avoid this non-tax challenge.”

Do you have a specific need for advice? Birgit Jürgensmann is at your disposal.

The rapid spread of COVID-19 (coronavirus) has presented every business with extraordinary challenges when it comes to personnel, social and economic issues in a very short space of time. As of now, it is difficult to predict just how far-reaching the effects of the crisis will be. However, it is clear that it will have serious consequences for businesses and for our society as a whole. Economists...

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.