Contact

Our last study, How are major European construction groups performing?showed an average return of between 2.6% and 8.9% annually over the last ten years for our sample of 15 European groups.

This sector certainly presents its own particular risks, but it also has a number of attractions: a certain stability in the levels of results, average growth prospects of 4.1% annually until 2020, the impact of emerging countries with their keen demand for infrastructure, and a still-significant fragmentation in the sector (given that the 15 majors represent 12% of the European construction market), suggesting that there is scope for consolidation.

In additional to the analyses conducted for mergers and acquisitions and due diligence operations in this sector, we have talked to financial analysts and studied brokers’ reports on the listed values for our sample. The valuation of the concession business, which is based on specific business models, and of other activities (telephony, etc.) that are not connected with the construction industry have not been included in our analyses.

Source : Aswath Damodaran

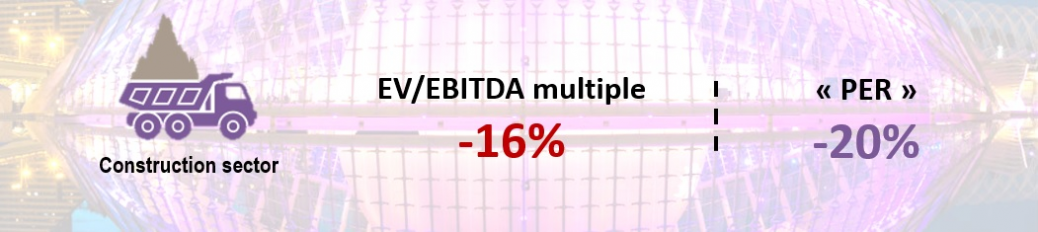

The levels of multiples for this activity remain lower than in other sectors. For the EBITDA multiple, the difference between the Engineering/Construction sector and the market average for all sectors is -16%. In the European zone alone, the valuation gap is similar, with a difference of -13% for the sample of 170 European Engineering/Construction entities.

For the Price Earnings Ratio (PER), we found a difference between the Engineering/Construction sector and the market average of -20%.

To find out more download our study below.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.